Currently viewing: Chief Financial Officer's Report / Next:Five-year Review

Chief Financial Officer's Report

“EOH is a good business with good value in our core businesses. We are integral to the SA business environment and we are committed and have a duty to drive the turnaround.”

Megan Pydigadu

Group Chief Financial Officer

Normalised EBITDA

SALIENT FEATURES

EOH affirms its commitment

to building a sustainable, agile

and competitive business

Many challenges faced

and progress made in

improving systems,

controls and culture.

Responsible deleveraging

plan agreed with lenders.

Deleveraging to occur into

calendar year 2021.

Continued disposal of

non-core assets in order

to build a sustainable

business into the future.

Q: What were your first impressions of EOH when you were appointed as CFO in January 2019?

I was very aware that it was going to be a challenging assignment. I just did not realise how challenging. The first half of the fiscal year prior to me arriving had been characterised with a strategic B-BBEE transaction which had also helped to address liquidity issues.

I started a month before Microsoft announced the cancellation of its licence agreement and after that everything changed. We were then catapulted into the ENSafrica investigation and the reputational issues arising therefrom. This also set us on a faster track in terms of creating transparency into the organisation and strategy as well as fast tracking the sale of non-core assets to create liquidity.

The business had also historically been overly focused on revenue and profit with a lack of focus on the balance sheet which became another significant area of focus as we set about cleaning up the balance sheet and ensuring that it represented reality and value.

Q: What are some of the actions you implemented to address this situation?

A lot more work than we initially anticipated was required around strategy, cleaning up the balance sheet and streamlining the capital structure. Project Offspring was established by EXCO and was designed to drive this work, simplify an overly complex group and enhance decision making. It focused on four key workstreams namely, people, governance, reorganisation and capital structure and liquidity.

The sale of non-core assets to create liquidity became a priority. From a credit and collection perspective, the management of working capital was crucial. We also implemented a cost efficiency drive across the business.

Considering where we started, we have made some really good progress in implementing a sound corporate structure and also enhancing our accounting systems and financial discipline across the organisation. The business did not have treasury, tax and financial planning and analysis ('FP&A') functions. These have been put in place together with skilled and resourced professionals.

The balance sheet we found did not represent reality and it has proven to be a monumental task to clean it up. We now have a far better understanding of the balance sheet and what represents value. We have driven accountability and ownership into the organisation and for the first time, we have a delegation of authority in place.

Over the longer term I would like to ensure we have created a high performance finance team that is innovative in its approach, adopting digitisation and ensuring we partner with business while at the same time representing the highest standard of ethical leadership.

Q: The business has been hit hard in respect of financial performance. Can you unpack this?

To start, it was important when preparing these results that we understood the technical complexities, the future strategy for the Group and could present this for users to give greater transparency.

EOH's revenue from continuing operations in the 2019 financial year was down 3% to R11 791 million (2018: R12 103 million). Gross margins for the year were 20% compared to 28% in the prior year. Revenue was negatively impacted by continued weakness in the economy, delays in infrastructure projects as well as the reputational impact of the cancellation of the Microsoft licence reseller agreement.

The margin decline was largely due to the impact of closing out large onerous contracts pertaining to complex ERP projects in the public sector and the closure of projects in the industrial technology area related to electrical infrastructure in the water sector. We have closed out the majority of these projects but still expect to see a small drag into the 2020 financial year as we close out the remainder.

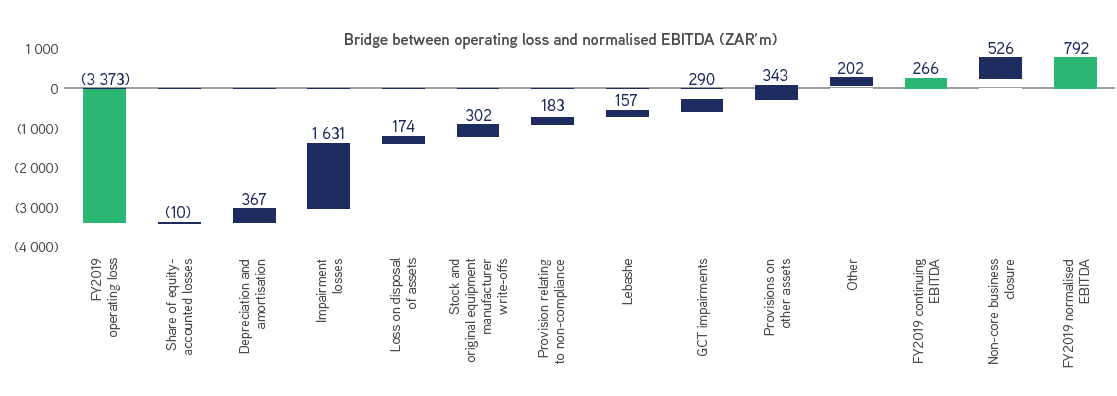

Operating expenses after stripping out once-off items for both years decreased to R2,6 billion in the 2019 financial period. Once-off items included impairment of assets of R2 263 million, a R157 million IFRS 2 charge related to the BEE transaction with Lebashe Holdco and its subsidiaries ('Lebashe') and settlements and provisions of R358 million among other once-off items.

Normalised EBITDA for the period amounted to R792 million (2018:

R955 million). The impact of the previously discussed once-off items and impacts on gross margin has resulted in a reduction in the profitability measures. Headline loss per share (HEPS) and loss per share (EPS) from continuing operations were 1 352 cents (2018: 728 cents) and 2 464 cents (2018: 1 277 cents), respectively.

Q: How did the underlying businesses perform?

The IP businesses including Sybrin, Syntell and Information Services continue to be our growth vector and achieved positive continuing revenue growth of 14% in the 2019 financial year and normalised EBITDA margin of 20%. This performance is supportive of our belief that we have high potential IP businesses with scaled technology.

NEXTEC posted positive revenue growth of 7% on a continuing basis, however, performance was impacted by delays in infrastructure projects and delivered a normalised EBITDA margin of 5%.

The iOCO business which is our traditional and core ICT offering was impacted by a drop in hardware sales directly related to reputational issues resulting in a slight revenue decrease in the current year. This has been one of the easiest places for our customers to change suppliers. It, however, still delivered normalised EBITDA margin of 8%.

Q: Can you expand on the work done to deleverage and clean up the balance sheet?

“The balance sheet we found did not represent reality and it has proven

to be a monumental task to clean it up. We now have a far better

understanding of the balance sheet and what represents value.”

Delivery on liquidity events enabled delivery of deleveraging in H2 2019

The Group has historically raised the vast majority of its funding centrally, with the funding largely used to drive the acquisition strategy with little regard or focus on the balance sheet. The repayment profile of the historic debt has not mirrored the cash-generation profile of the acquired businesses and as a result has placed strain on the Group. EOH is largely a service business with a light balance sheet that is unable to carry a large debt burden.

A deleveraging plan has been put in place to reduce the Group's debt through two primary focus areas being the sale of non-core assets and realising cash out of the debtors book.

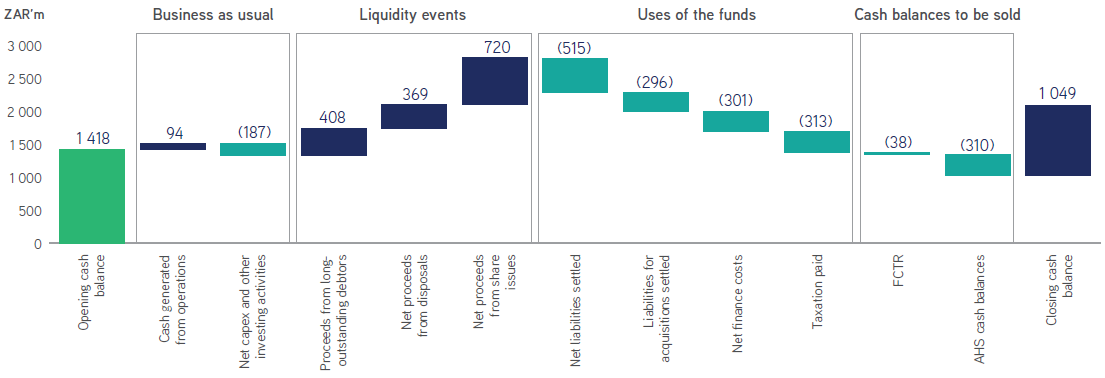

We have been successful in selling off non-core assets and finding a strategic partner for CCS which resulted in net cash realisation of R369 million.

ZAR’m

FY2019

HY2019

FY2018

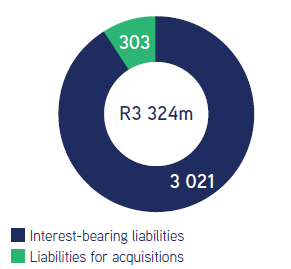

Interest-bearing liabilities

3 021

2 775

3 405

Cash and cash equivalents

1 359

957

1 418

Net debt

1 662

1 818

1 987

Liabilities for acquisitions

303

419

634

Net debt including liabilities for acquisitions

1 965

2 237

2 621

*

All balances include assets held for sale.

At the half year a target was set to significantly reduce the debtors balance. By 31 July 2019, the trade receivable balance decreased from R4,1 billion to R3,4 billion (before adjusting for current assets held for sale) with over R400 million cash realised from debtors' balances greater than 90 days at 31 January 2019.

By 31 July 2019 the Group was able to repay its bridge facility of R250 million taken out during the year. Going forward, we have agreed a plan with our lenders to deleverage our debt by R1,5 billion by 2021 primarily through the sale of non-core assets and finding strategic partners for our IP assets.

Gross liabilities (ZAR’m)

Q: Could you explain the qualification of the opening balance sheet?

When I joined EOH less than a year ago, it became evident that the organisation had historically placed a strong focus on growth in revenue and profit to the detriment of careful balance sheet management, with a lack of presentation or analysis of monthly balance sheets at EXCO meetings and the review of the Group balance sheet only twice a year with the release of our interim and annual results. For this reporting period ended 31 July 2019, our primary focus was to ensure we had a closing balance sheet that provided a credible basis upon which investors and shareholders could make decisions.

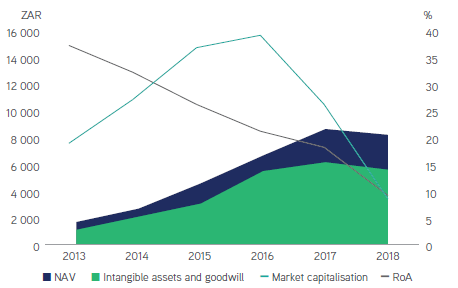

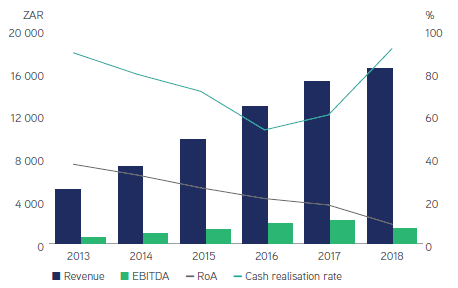

The fact that EOH's balance sheet shrank from R8,1 billion to R1,9 billion in the space of less than a year suggests that there was more at play than simply a different outlook and increased focus by new management on the strength of the balance sheet. This reduction in net asset value suggests something far more fundamental in terms of weaknesses in the application of accounting policies and interpretations in prior periods. For many of the adjustments identified, we found that there were already indicators when looking at historic performance. This is demonstrated in the graphs below.

Declining RoA on increasing NAV

Increasing revenue and EBITDA versus declining RoA and cash realisation

During the current reporting period, we identified various transactions that spanned different accounting topics, including revenue recognition, asset capitalisation and subsequent recovery, the timing of the recognition of liabilities and the recognition of impairment losses.

In assessing whether the identified adjustments should be processed as prior period errors or in the current reporting period, we considered whether the facts that gave rise to the adjustments existed in prior years, or whether those events only arose due to information that came to light in the current year. We only processed adjustments as prior period errors if the facts that gave rise to the adjustment were found to clearly have existed in prior years.

It is important to clarify that items deemed to be prior period errors do not merely result from the new EOH management team applying different judgement to the prior management team, but rather from the application of IFRS accounting principles to prior year transactions using information that existed at that time. If there was any uncertainty about whether the events that gave rise to an accounting adjustment existed in the prior period, we processed the accounting adjustment in the current year.

Measurement of these prior period errors did in some cases require management to make estimates; as set out in paragraph 53 to IAS 8 – Accounting Policies, Changes in Accounting Estimates and Errors, the fact that significant estimates are frequently required when amending comparative information presented for prior periods does not prevent reliable adjustment or correction of the comparative information.

We understand both the magnitude of adjustments of the prior period errors and the challenge of assessing adjustments to prior periods without the use of hindsight, and reiterate that we believe the adjustments processed to prior periods resulted from the application of accounting guidance to the facts and circumstances that existed at the time.

Regardless of the decisions taken by our predecessors, in principle, it is critical for us to be transparent now, and to ensure that even though we may disagree with our external auditors on aspects of timing for certain of these adjustments, we believe it is right to stand by our assessment of the facts and circumstances available at the time.

Q: What is your outlook for the year?

EOH is a great business with good value and potential. We are integral to the South African economy and we are committed and have a duty to drive the turnaround. We are ideally placed to play a significant role in the fourth industrial revolution. The coming year will continue to be a refinement of our strategy, reassessing and selling off non-core assets as well as ensuring we have a fit-for-purpose cost and debt structure.